An Overview of the Canada Pension Plan Maximums 2024

As a Canadian taxpayer, it’s essential to understand your CPP max for 2024. The Canada Pension Plan (CPP) contribution rates for employees and employers in 2024 will be 5.95%, unchanged from 2023, while the self-employed contribution rate for CPP will remain at 11.90%.

This blog post offers an overview of key information related to CPP contributions.

Key Takeaways

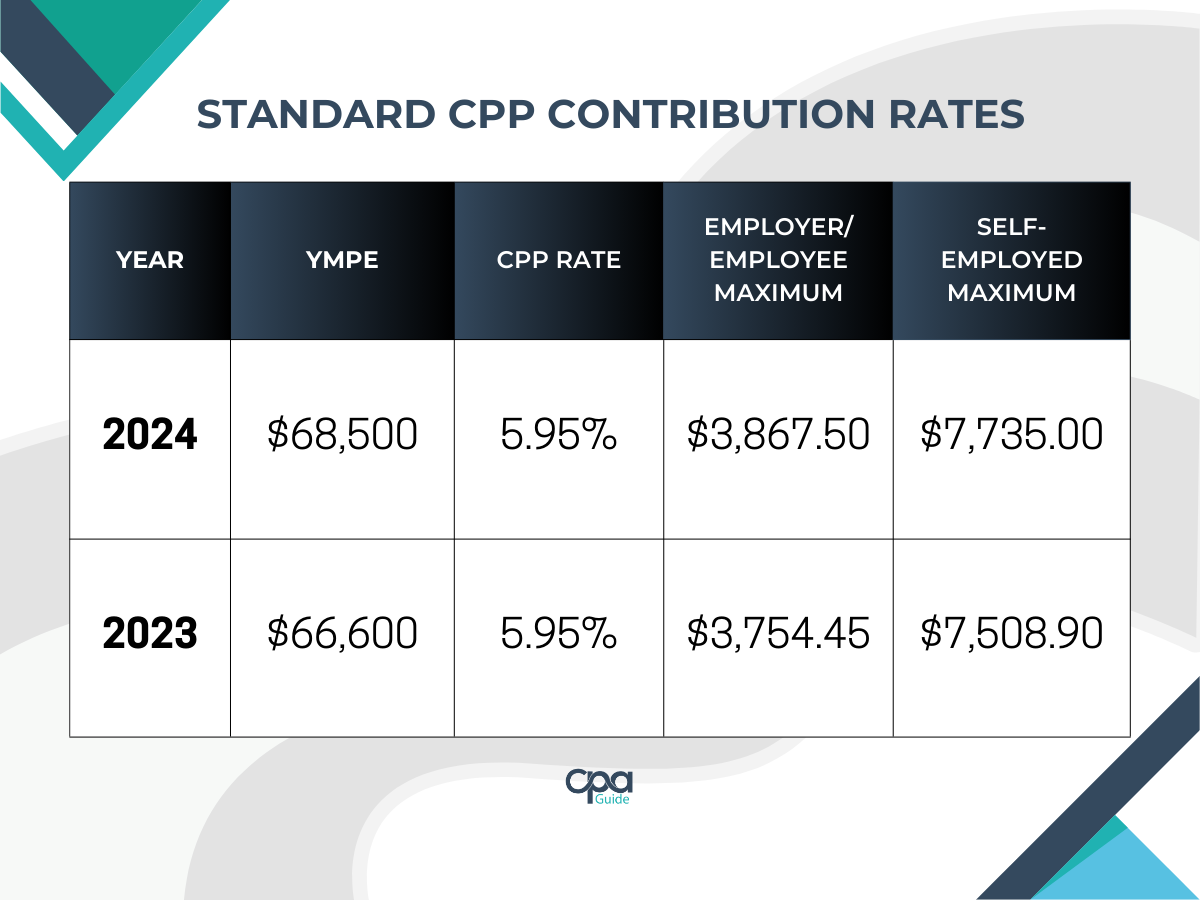

- The CPP max 2024 contribution rate will remain at 5.95% for employees and employers and 11.90% for self-employed persons, with maximum pensionable earnings set at $ 68,500.

- Self-employed individuals must pay employee and employer portions of their CPP max contributions and ensure they stay within the maximum pensionable earnings of $68,500 to avoid additional funds come the 2024 filing season.

- It is crucial that Canadian taxpayers adequately budget for any potential increases in CPP payments they may owe according to changes imposed for 2024 while seeking professional financial advice when necessary to optimize their retirement savings goals through informed decisions during 2024 or beyond.

CPP Contribution Rates And Maximums For 2024

Canada Pension Plan has introduced a new, new, higher earnings limit for 2024. Hence, there will be two tiers CPP max contribution rates: the standard CPP contribution rates and the second earnings ceiling.

This only means that if you earn between $68,500 and $73,200, you’ll have to pay CPP2 contributions.

CPP Payments: Two-Tiered Contribution Rates

Starting in 2024, the CPP (Canada Pension Plan) will have a system with two-tiered contribution system:

- First Earnings Ceiling (YMPE): This is the standard CPP contributions. The year’s maximum pensionable earning (YMPE) for 2024 is at $ 68,500. The standard CPP rate for employees and employers is 5.95% and 11.9% for self-employed.

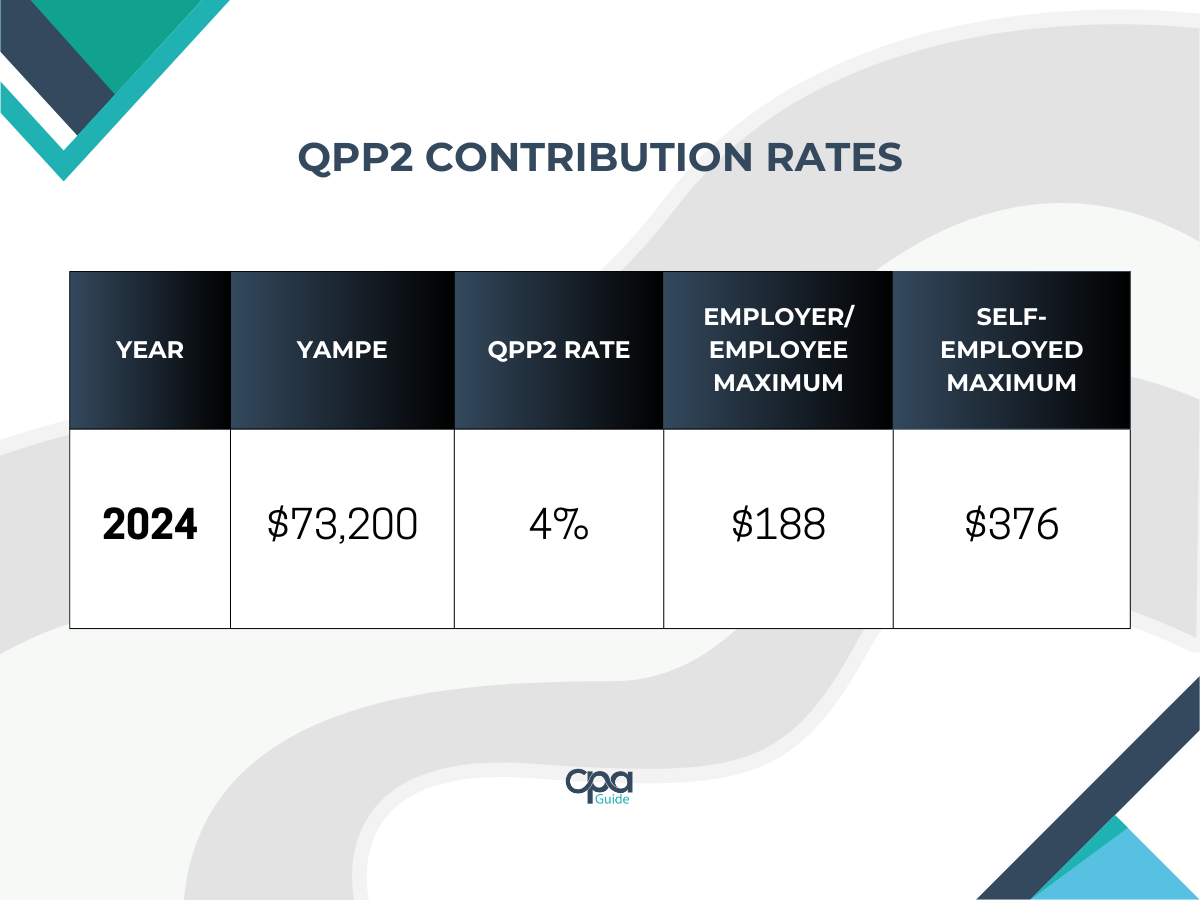

- Second Earnings Ceiling (YAMPE):This is the upper limit for the second tier of CPP max contributions. In 2024, the year’s additional maximum pensionable earning (YAMPE) is 7% higher than the YMPE, a total of $73,200. The CPP2 rate for employees and employers is 4% and 8% for self-employed.

How Do CPP and CPP2 Apply To You?

Standard CPP: Year’s Maximum Pensionable Earnings (YMPE)

Under the Canada Pension Plan in 2024, Canadians can contribute up to a year’s maximum pensionable earnings (YMPE) of $68,500. It is higher than the MPE set for 2023, which was $66,000.

How to calculate your CPP max 2024 contribution

Formula:

(YMPE – Basic Exemption) CPP2 Contribution Rate = Your Maximum Contribution

CPP2: Year’s Additional Maximum Pensionable Earnings (YAMPE)

Under the CPP2, Canadians can contribute up to a year’s maximum pensionable earnings (YAMPE) of $73,200.

How to calculate your CPP2 max 2024 contribution

Formula:

(YAMPE – YMPE) Contribution Rate = Your Maximum Contribution

So, if you’re earning between $68,500 and $73,200, the total CPP payments you’ll make in 2024 are the maximum contributions for both the YMPE and YAMPE.

People who earn more than the YAMPE don’t have to or can’t pay extra CPP contributions.

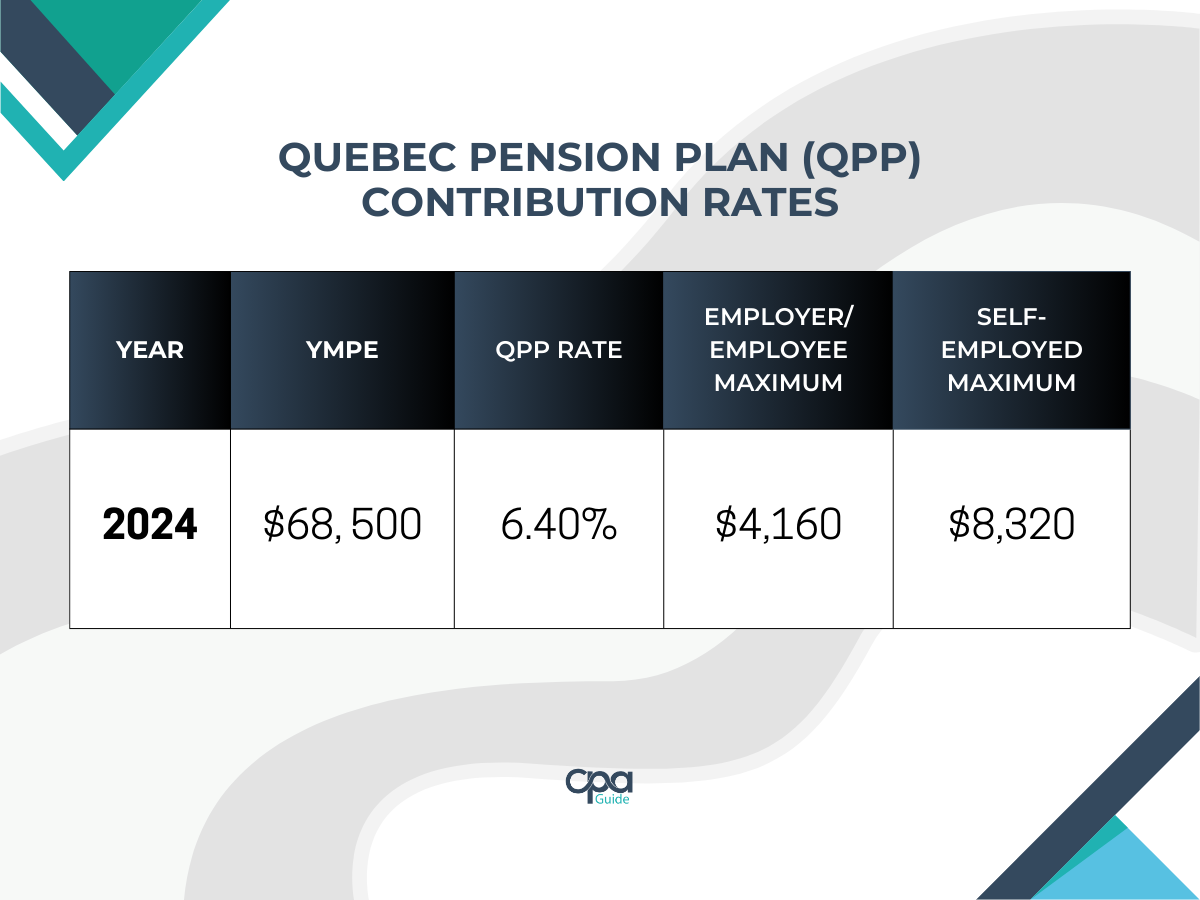

Quebec Pension Plan (QPP) Contributions for 2024

The Quebec Pension Plan (QPP) figures for 2024 are:

Meanwhile, these are the figures for the QPP2:

3 Ways To Prepare For CPP Contribution Changes In 2024

With the changes to CPP contribution rates for 2024 already announced, employees should start preparing to avoid surprises next year.

- Budgeting For Increased Contributions

Canadian taxpayers must consider how they will budget for increased contributions in preparation for the CPP enhancements. While considering these changes when creating their budgets, you can also factor additional tax exemptions or deductions that may be applicable that year to increase financial stability amid the contribution increases.

- Planning For Maximum Pensionable Earnings

As 2024 approaches, Canadian taxpayers must understand the applicable CPP and CPP2 contribution rates and how they may be affected by exceeding the year’s maximum pensionable earnings. Exceeding this limit can have a significant impact on contributions as well as retirement income.

Here are several key points to consider when planning:

- Employees and employers must pay contributions on all earned income between $3,500 and the YMPE. Should an employee exceed that amount, then employer contributions cease. However, additional employee contributions will still be required until their annual salary is reached or any other limit set by taxable earnings from self-employed work that year.

- Your maximum CPP payments will depend on how much you contribute throughout your working life (measured from age 18). Therefore exceeding a certain YMPE ceiling for one particular fiscal period could diminish your overall benefits in retirement years unless adequate provisions are made through contributing personal funds into RRSP or TFSA accounts separately outside the company structure.

- It’s possible to opt out of contributing towards CPP if you do not wish to receive its benefits later; however, this should only be done after diligent consultation with financial advisors/government officials prior decision-making process commence please due to understanding local laws surrounding the capital gains taxation policies etc. beforehand take priority always!

- Seeking Professional Financial Advice

Seeking the assistance of a financial advisor can be an invaluable resource when planning for CPP max 2024 contribution changes. A qualified professional can help individuals understand their rights and responsibilities associated with contributing to the CPP and recommend strategies for achieving their goals.

Financial advisors are especially helpful in outlining any potential exemptions or reductions that may apply in 2024, such as those related to childcare costs and disability benefits, so taxpayers don’t miss out on saving opportunities or pay too much into the plan.

Finding a personal income tax accountant is really advantageous if you really want to prepareyour contributions.

READ MORE: The Ultimate Guide to Finding Accounting and Tax Services in Canada

CPP Max 2024 Payment Dates

Here are the 2024 CPP payment dates:

- January 29, 2024

- February 27, 2024

- March 26, 2024

- April 26, 2024

- May 29, 2024

- June 26, 2024

- July 29, 2024

- August 28, 2024

- September 25, 2024

- October 29, 2024

- November 27, 2024

- December 20, 2024

CPP Exemptions And Reductions In 2024

Exploring the applicable exemptions and deductions related to CPP in 2024 could help you identify ways to minimize your tax burden.

Applicable Exemptions And Deductions

This section will discuss the various exemptions and deductions that may apply to Canadian taxpayers concerning CPP contributions. Understanding these exemptions and deductions can help individuals and businesses plan their financial strategies more effectively. Below is a table outlining the key exemptions and deductions that may impact your CPP contributions.

Each of these exemptions and deductions can have a significant impact on the CPP contributions of Canadian taxpayers. It is essential to know their eligibility and how to claim these to make informed financial decisions and reduce the overall burden of CPP contributions.

Impacts of CPP Max 2024 Contributions

Impacts On Employee And Employer Contribution

The CPP contribution rate stays the same at 5.95% this year. However, the maximum amount of earnings that count towards your pension has gone up to $68,500.

There’s also something new called CPP2. If you earn between $68,500 and $73,000, you’ll have to chip in an extra 4% of your income.

So, if you’re in the CPP2 bracket, you’ll be paying more overall towards your CPP contributions. Employers have to put in more money to match what their employees are contributing to the CPP (Canada Pension Plan), which means they’ll have higher costs for running payroll.

Impacts on Self-employee Contributions

Self-employed individuals cover both the employee and employer portions of CPP contributions. As a result, the self-employed contribution rate for this added range (CPP2) will be 8%.

Conclusion

Understanding CPP contribution rates, maximums, and exemptions for 2024 is essential to ensure Canadians are adequately prepared for changes in their retirement-saving contributions.

Individuals who fall within the range of taxable income should plan and budget for any increases to CPP payments they may owe to avoid potential penalties or interest charges from the CRA.

Additionally, those pursuing self-employment should be aware of their responsibility to contribute both as an employee and employer, which can result in greater savings come retirement age.

Frequently Asked Questions about the CPP maximum 2024

1. What are defined contribution rates and maximums under the Canada Pension Plan?

The contribution rate is the percentage of an individual’s income that must be contributed to CPP each year up to a certain contribution rate limit (also known as ‘maximum’). For 2024, this contribution rate is estimated at 5.95%, with a maximum of $68,500 in contributions required.

For the CPP2, the contribution rate of 4% with a maximum pensionable earnings of $73,200.

2. Are there any exemptions granted for CPP contributions?

Yes – some individuals may qualify for an exemption from contributing to CPP if they receive disability benefits or qualify for other exceptions as noted by Canada Revenue Agency stipulations. Additionally, people between the ages 60-65 will not have to contribute if either retired or continue working without exceeding seasonal frequency limitations set out on their website or those indicated via service providers such as payroll departments within companies they work/used to work with.

3. Do Canadians outside Canada still need to pay into CPP?

Yes – Canadians residing outside of Canada, when receiving employment income within it, will still need pay based on policies stated above unless exempted due to contractual agreement(s) established before moving overseas and verified by the employer/payroll institution who processed said sums while a person was away from home country etc. It is always best advised to consult a lawyer for more information.

4. How often should I check my CPP contributions?

It is important to review your statements regularly and double-check them against your current earnings, so you know precisely how much you owe and whether you are overpaying or underpaying your monthly premiums etc.

Are you in need of a reliable Canadian accountant to assist with the growth and management of your business? Look no further than CPA Guide! We have conducted thorough research to provide excellent CPA and accounting services to help your business flourish. Find a CPA today with CPA Guide.